The Impact of Credit Card Interest Rates on Consumer Financial Health

The Importance of Credit Card Interest Rates

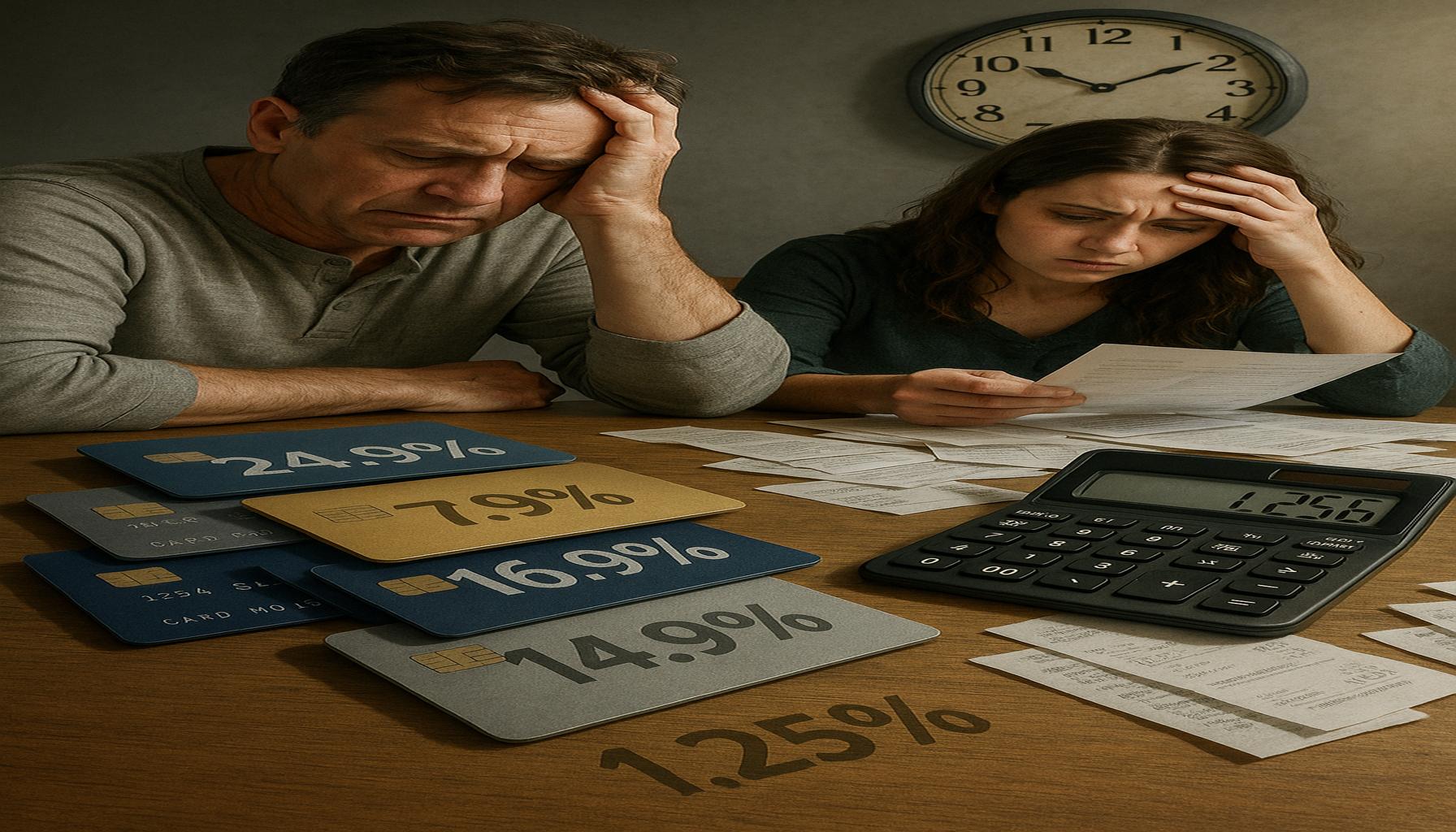

Credit card interest rates are a pivotal element in personal finance, influencing an individual’s ability to manage and repay debt. Understanding how these rates function is essential for consumers seeking to maintain financial stability. The rates applied to credit card balances can significantly impact monthly payments and overall financial health.

High interest rates can lead to substantial burdens on consumers, creating a cycle of debt that is difficult to escape. Key consequences of elevated interest rates include:

- Increased Debt: When interest rates are high, the cost of borrowing increases, causing outstanding balances to grow more rapidly. For example, if a consumer carries a balance of $5,000 with an annual percentage rate (APR) of 20%, they could accrue approximately $1,000 in interest over the course of a year if they make only minimal payments.

- Longer Repayment Periods: Consumers faced with high interest may struggle to pay down their principal balance. As a result, they may extend their repayment periods, incurring further interest charges. This prolongation not only increases the overall cost of debt but can also create financial stress.

- Impact on Credit Scores: A high utilization rate from carrying large credit card balances can lead to a drop in credit scores. Credit bureaus typically prefer that consumers use less than 30% of their available credit; exceeding this threshold can flag accounts as risky, leading to potential difficulties in obtaining loans or favorable interest rates in the future.

Various factors influence how credit card interest rates are determined, which is vital for consumers to understand. Key determinants include:

- Credit Score: A higher credit score generally helps secure lower interest rates. Individuals with scores above 740 typically qualify for some of the best rates offered, while those with lower scores may face significantly higher interest charges, affecting their overall financial landscape.

- Economic Conditions: The broader economic environment can impact credit card interest rates as well. For instance, during periods of economic growth, interest rates may increase due to higher demand, while recessions often see rates decrease as consumers become more financially cautious.

- Card Issuer Policies: Each credit card issuer may adopt its own criteria for setting interest rates, which can vary widely based on their risk assessment and market positioning. Consumers should carefully review multiple offers to find competitive rates tailored to their creditworthiness.

By closely examining these factors, consumers can make informed decisions regarding their credit card use and financial strategies. Recognizing the potential repercussions of high interest rates empowers individuals to take proactive steps in managing their finances. For instance, individuals may consider strategies such as transferring balances to cards with lower rates, making more than the minimum payment, or utilizing financial planning tools to create a budget that prioritizes debt repayment. Such measures can effectively mitigate the adverse effects of high credit card interest rates, leading to a healthier financial life.

DISCOVER MORE: Click here for safe investment tips

The Consequences of High Credit Card Interest Rates

The implications of high credit card interest rates extend beyond mere monthly payments; they can significantly affect a consumer’s overall financial health and well-being. As individuals increasingly rely on credit cards for a variety of purchases, understanding the potential risks associated with elevated interest rates becomes crucial. Several key repercussions of carrying high-interest credit card balances warrant attention:

- Financial Stress: High credit card interest rates can contribute to mounting financial stress. Consumers may find themselves juggling multiple payments while also dealing with the anxiety of an increasing balance. This stress can have serious implications not just for financial health, but for physical and mental well-being as well.

- Limited Financial Flexibility: As a consumer allocates more of their monthly income to servicing credit card debts, they may find themselves with limited financial flexibility. This situation restricts their ability to save for emergencies, invest in future opportunities, or even afford essential expenses, potentially endangering their long-term financial objectives.

- Risk of Default: With growing debt burdens and interest payments, the risk of default increases significantly. Missing payments or accruing late fees not only exacerbates the situation but can also lead to severe consequences such as damage to credit scores and additional legal complications.

In the context of these repercussions, it is essential to recognize the broader implications of credit card interest rates on consumer behavior. Many consumers may resort to relying on credit cards for emergencies or substantial purchases, often leading to higher debt accumulation. This reliance on credit can be exacerbated during challenging economic times, where unexpected expenses may arise. Consequently, individuals who experience high interest rates may find it increasingly difficult to break the cycle of debt, as the cost of borrowing continues to rise.

Moreover, consumers often lack awareness of how high interest rates influence their financial scenarios. Many may not fully grasp the concept of compounding interest and how it can significantly inflate outstanding balances over time. For instance, a consumer who consistently carries a balance may end up paying much more than the original amount borrowed due to high interest rates, thus prolonging their financial burden.

Recognizing these consequences is the first step towards improving consumer financial health. Sufficient knowledge about interest rates enables consumers to make informed decisions about their credit card usage. Making strategic choices, such as actively comparing different credit card offers before committing, can result in lower interest rates. This proactive approach allows individuals to mitigate the adverse impacts of high credit card interest rates, thereby promoting better financial health and stability.

DIVE DEEPER: Click here to learn how to invest wisely

The Role of Consumer Behavior and Understanding in Mitigating Risk

Understanding the dynamics of credit card interest rates is not only about recognizing their immediate effects on monthly payments; it also encompasses how consumer behavior can either exacerbate or alleviate financial challenges. A clear comprehension of credit terms and responsible usage can greatly influence a consumer’s financial trajectory. Several factors and considerations highlight the importance of informed consumer behavior in the context of credit card management:

- Budgeting and Spending Habits: A disciplined approach to budgeting can greatly mitigate the impact of high-interest credit card debt. Consumers should establish and adhere to a detailed budget that separates needs from wants, allowing for strategic credit card usage that aligns with their financial capabilities. Studies suggest that individuals who actively track their spending and prioritize essential expenses tend to maintain lower credit card balances and avoid high-interest pitfalls.

- Understanding APR and Fees: Many consumers are often unaware of the terms beyond just interest rates, such as the annual percentage rate (APR) and associated fees. A Consumer Financial Protection Bureau (CFPB) report reveals that nearly 40% of consumers do not know their credit card’s APR. Understanding these figures allows consumers to make educated choices when selecting credit cards and help avoid incurring unnecessary debt through hidden fees.

- Utilizing Grace Periods: Many credit cards offer a grace period during which no interest is charged if the balance is paid in full before the due date. By taking advantage of this feature, consumers can avoid interest fees altogether on new purchases. However, reliance on minimum payments can lead to prolonged debt and increased interest accumulation, which underscores the importance of financial literacy.

Additionally, consumers often overlook the potential for transferring existing balances to credit cards with lower interest rates. Such balance transfer offers, often presented as promotional rates, can provide temporary relief from high-interest payments. According to TransUnion data, consumers who transferred balances onto low-interest accounts experienced a average reduction of over 20% in their monthly payments. While these offers can be beneficial, it is important for consumers to be aware of the terms and any potential fees that may apply after the promotional period ends.

Moreover, the role of financial education cannot be overstated. Programs aimed at enhancing financial literacy equip individuals with the knowledge necessary to navigate the complexities of credit, including interest rates. A 2021 survey by the National Endowment for Financial Education indicated that individuals who participated in a financial literacy program reported a 55% increase in confidence regarding their credit management abilities. By investing time in understanding credit card terms, consumers are better positioned to make choices that align with their financial health.

Finally, a theme emerges around the psychological aspects of using credit cards. The ease of swiping a card for purchases can lead to overspending and an unmanageable accumulation of debt. Awareness of this behavior is essential for consumers seeking to maintain financial stability. Techniques such as the “50/30/20 rule,” where 50% of income is allocated to needs, 30% to wants, and 20% to savings or debt repayment, can empower consumers to strike a balance and mitigate adverse effects of high interest rates.

DIVE DEEPER: Click here to uncover smart investment strategies

Conclusion

In light of the significant influence that credit card interest rates exert on consumer financial health, it becomes crucial for individuals to cultivate a robust understanding of credit management practices. The high cost of borrowing, driven by elevated interest rates, can lead to a cycle of debt that negatively impacts financial stability. However, through informed consumer behavior, the adverse effects of these rates can be mitigated.

Adopting effective budgeting strategies and recognizing the intricacies of APR and associated fees can empower consumers to make better financial decisions. The intentional use of credit cards, taking advantage of grace periods and balance transfer offers, further exemplifies how proactive management can alleviate the burden of high-interest payments. Financial literacy initiatives play a pivotal role in equipping consumers with the necessary tools to navigate credit complexities, fostering confidence and competence in their financial decision-making.

As consumers become more aware of their spending behaviors and the psychological aspects tied to credit card usage, they can pave the way towards healthier financial outcomes. Emphasizing practices such as the “50/30/20 rule” not only promotes effective budgeting but also establishes a foundation for sustainable financial health. In conclusion, while credit card interest rates remain a critical concern, the onus lies with consumers to educate themselves, adapt their behaviors, and proactively manage their credit to ensure long-term financial well-being.